Do you ever feel like your paycheck disappears just days after it hits your account? You’re not alone. While many people build their budgets around a monthly schedule, over 43% of Americans are actually paid every two weeks. That means 26 paychecks per year—not 24 or 12. By using a bi-weekly paycheck budgeting strategy, you can better align your money with your lifestyle and unlock hidden savings opportunities. It’s a smarter, more agile way to manage your cash flow.

Financial Toolkit / Essentials

To successfully implement a bi-weekly budget, you’ll need the right tools and mindset:

- Budgeting Apps with Paycheck Features: YNAB, EveryDollar, and Monarch Money support paycheck-based planning.

- Calendar App or Printable Pay Schedule: Helps map out income and bills.

- Two-Account System: One account for fixed bills, one for variable spending.

- Sinking Fund Tracker: Use Google Sheets or Goodbudget to save gradually for irregular expenses.

- Bill Due Date Tracker: Use Truebill or a simple spreadsheet to monitor recurring charges.

Personalization Tip: Match your budgeting app to your habits. If you like automation, go with apps like YNAB or Monarch. If you prefer manual control, Google Sheets gives total flexibility.

Time Commitment / Planning Horizon

Budgeting bi-weekly is efficient and rewarding with consistent check-ins:

- Initial Setup (1-2 hours): Analyze income, expenses, and schedule your first two paychecks.

- Bi-Weekly Planning (30 minutes per paycheck): Allocate funds, refill categories, and pay bills.

- Monthly Review (30 minutes): Adjust for overspending, upcoming events, or changes in income.

Compared to monthly budgeting, bi-weekly gives you more flexibility and faster feedback.

Step-by-Step Instructions

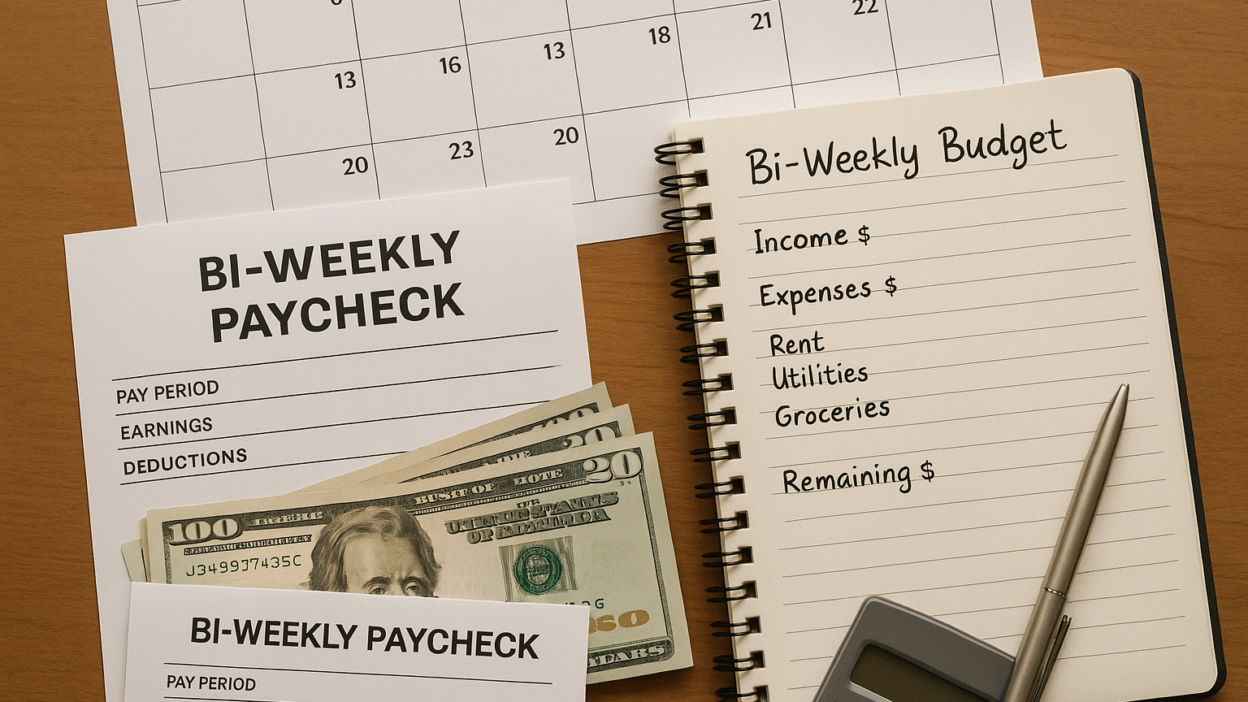

Step 1: List Your Fixed Expenses

Write down monthly bills (rent, utilities, car payment, etc.). Divide each total in half to allocate across two checks.

Step 2: Identify Variable Expenses

Groceries, gas, entertainment, and dining out are better handled with spending caps per paycheck.

Step 3: Align Bills with Paydays

Use a calendar to match due dates with paycheck arrival. If needed, call providers to shift due dates.

Step 4: Build a Paycheck Plan

For each paycheck:

- Allocate half of your rent/mortgage

- Fund groceries, gas, and other essentials

- Save toward monthly or irregular costs (e.g., holidays, subscriptions)

Step 5: Use the Two Extra Paychecks Strategically

A bi-weekly schedule gives you two extra paychecks per year (usually in months with 3 paydays). Use these to:

- Boost emergency savings

- Pay down debt

- Invest in retirement or education

Pro Tip: Treat those two extra checks as a bonus, not spendable income.

Key Financial Metrics

- Average U.S. bi-weekly income after tax: $1,500–$2,300 (varies by location and job)

- Median rent in U.S.: ~$1,372/month, or ~$686/paycheck if split

- Extra paycheck months (2025): May and October (for Friday pay cycles)

Tracking these metrics helps you plan precisely and stay ahead of your expenses.

Smarter Alternatives

- 1-1-1 Rule: Spend 1/3 on needs, 1/3 on wants, 1/3 on future you (savings or debt).

- Reverse Budgeting: Save first, then allocate remaining funds to spending.

- Zero-Based Budgeting: Assign every dollar a job before you spend.

- Budget by Week Instead of Paycheck: Helpful if expenses are irregular.

Application Scenarios

- Teacher Paid Bi-Weekly: Uses YNAB to track pay periods and allocates toward summer expenses during the school year.

- Freelancer Paid Sporadically: Converts income to a bi-weekly system for consistency.

- Retail Worker with Varying Hours: Budgets fixed costs by half, then caps flexible categories with each paycheck.

Common Mistakes to Avoid

- Treating Extra Paychecks as Disposable Income: Plan in advance how you’ll use them.

- Ignoring Bill Due Dates: Leads to missed payments or late fees.

- Overestimating Variable Income: Always use the lower end of your income range.

- Failing to Build Sinking Funds: Irregular expenses derail bi-weekly budgets fast.

Maintenance & Optimization Tips

- Set bi-weekly calendar alerts to plan your paychecks.

- Use automated transfers for savings and bills.

- Keep a “cash buffer” for surprise costs between pay periods.

- Review and revise every 90 days to adjust to seasonal expenses or changes in income.

Conclusion

Switching to a bi-weekly paycheck budgeting strategy empowers you to manage your finances with precision and less stress. Whether you live paycheck-to-paycheck or want to optimize your extra checks, this approach helps you stay organized, avoid surprises, and achieve your financial goals faster.

💡 Want a free bi-weekly budget template? Download it now at YourFinanceWorld.com and start your paycheck-to-paycheck plan with confidence.

FAQs

1. How do I find out which months have three paychecks? Use a bi-weekly pay calendar or online calculator based on your pay schedule.

2. Should I save half my rent from each paycheck? Yes! That’s a key advantage of bi-weekly budgeting—you break up large bills into manageable chunks.

3. Can I do this with inconsistent income? Absolutely. Just base your budget on your lowest expected paycheck and build flexibility from there.

4. How do I manage subscriptions that hit monthly? Use sinking funds. Save 1/2 of the cost from each paycheck to cover monthly charges.

5. Is bi-weekly budgeting better than monthly? For many, yes. It reduces timing issues and improves cash flow control.