Personal Finance Basics

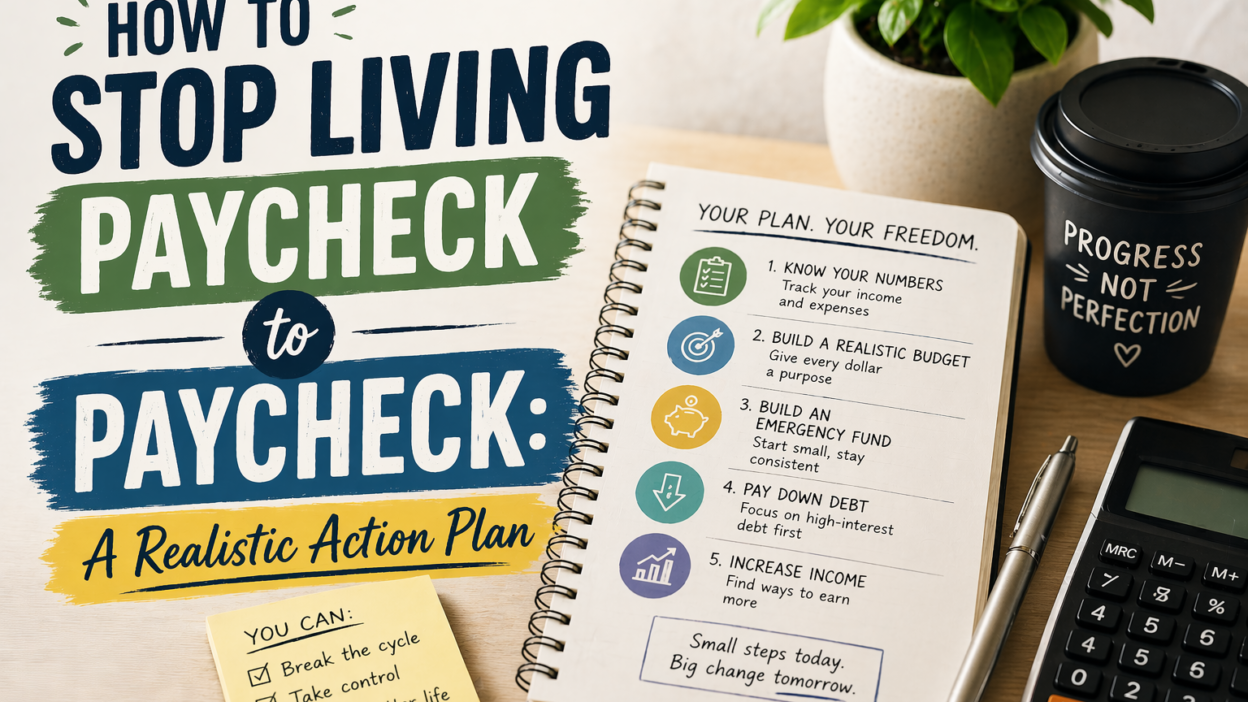

How to Stop Living Paycheck to Paycheck: A Realistic Action Plan

If you’re earning a decent salary but still running low on money before your next payday, you’re not alone. Studies show that a majority of Americans live paycheck to paycheck — regardless of income level. The problem usually isn’t how much you earn. It’s how money flows in and out.

Here’s a step-by-step plan to break the cycle for good.

Step 1: Understand Why It’s Happening

Before you can fix the problem, you need to diagnose it. Living paycheck to paycheck usually comes from one of three causes:

- Spending equals (or exceeds) income — lifestyle inflation keeps pace with every raise

- No financial buffer — unexpected expenses derail an otherwise balanced budget

- Debt payments eating income — credit card minimums, loans, and interest drain cash flow

Identify which one (or combination) applies to you — then tackle it directly.

Step 2: Create a Spending Gap

The only way out is to spend less than you earn — consistently. This “spending gap” is what you use to build savings and pay down debt.

You can widen the gap two ways:

- Cut expenses: Cancel unused subscriptions, negotiate bills, cook at home more, downgrade where possible

- Increase income: Ask for a raise, pick up freelance work, sell unused items, monetize a skill

Even a $200/month gap changes everything over time.

Step 3: Build a $1,000 Starter Emergency Fund

Most financial emergencies that derail people cost under $1,000. A car repair, a medical copay, a broken appliance. Before anything else, save a $1,000 buffer in a separate savings account.

This one step stops the cycle from repeating itself every time life throws a curveball.

Step 4: Automate Your Finances

Willpower runs out. Automation doesn’t. Set up your money to move automatically on payday:

- Auto-transfer a set amount to savings the day you get paid

- Auto-pay all fixed bills so you never miss a payment

- Use a separate checking account for discretionary spending — when it’s empty, spending stops

The goal is to make the right financial behavior the path of least resistance.

Step 5: Attack High-Interest Debt

If debt payments are draining your paycheck, that’s the bottleneck. Focus extra payments on your highest-interest debt first (the avalanche method). Every dollar of debt you eliminate frees up cash flow permanently.

Avoid taking on new debt while you’re in this phase — especially credit cards for non-essentials.

Step 6: Grow the Gap Over Time

As you pay off debt and build habits, your monthly breathing room will grow. When it does, resist the urge to inflate your lifestyle — redirect that money to your emergency fund, then to investing.

The goal isn’t just to survive until payday. It’s to get to a place where you’re a month ahead — paying this month’s bills with last month’s income.

The Bottom Line

Breaking the paycheck-to-paycheck cycle doesn’t happen overnight — but it does happen. It takes a clear plan, small consistent actions, and the discipline to close the gap between what you earn and what you spend. Start with one step this week.

Want more tips like this? Explore more Personal Finance Basics articles at YourFinanceWorld.com